Volume 10 – Opinions of Counsel SBRPS No. 21

NYS Real Property Tax Law, §§ 520, 553: [ Click Here To Read Legal Opinion Online ]

Exemptions, generally (transfer to non-exempt owner) (assessment review); Correction of errors (generally) (judicial review) – Real Property Tax Law, §§ 520, 553:

Where formerly exempt property is transferred to a non-exempt owner and is reassessed as of the date of such transfer, that reassessed value is subject to administrative and judicial review.

Section 520 of the Real Property Tax Law provides for the imposition of a pro rata tax liability when property receiving wholly or partially tax exempt status is transferred to a non-exempt owner after taxable status date. When such a conveyance occurs, the assessor, “shall forthwith assess such property at its value as of the date of transfer . . . and shall notify the new owner of the assessment and of the right of that owner to a review of the assessment . . . as provided by title three of article five of this chapter” (§ 520(2)). The question is as to the extent of this review.

The county/town tax year begins on January 1st. The school tax year starts on July 1st.

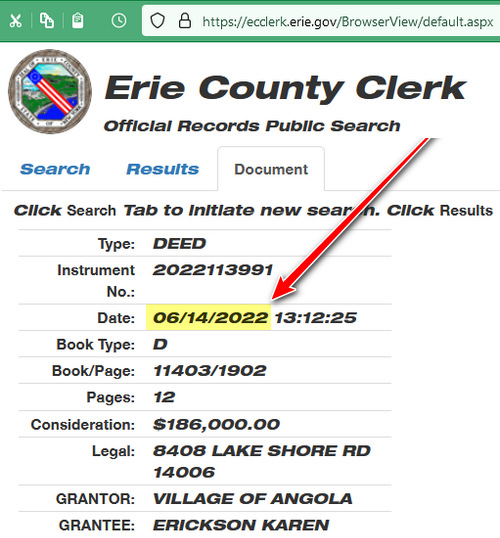

The closing date on 8408 Lake Shore Road was 6-14-2022. This means that Karen Erickson owes prorated county/town taxes from 6-14-2022 to 12-31-2022 and school taxes from 6-14-2022 to 6-30-2022 plus 100% of the 2022 school tax due.

https://ecclerk.erie.gov/BrowserView/default.aspx